Social Factor round-up

Worker-centred RI, Musk's passions and interests, BP / Elliott (again)

It has surprising to many how easy it has been for the Right in US to push back on Responsible Investment and how it has managed to turn people against a cartoon villain version of ESG.

Here’s a prediction: if they choose to do it, it will be easy for far/populist Right parties in Europe to attack ESG/RI as practised by many asset owners in the similar terms as those used in the US.

You can write the UK version of the critique now:

Our pension funds have been taken over by people who have put their own ESG preferences ahead of the interests of British savers. They want to shut down industries that still employ thousands of British workers and they only care about ‘equity’ when it comes to career advancement for middle class professionals and getting well-paid jobs on company boards. They don’t lift a finger for the ordinary Britons that pay their substantial wages. British pension funds should support British workers. We should DOGE the ESG industry feeding off our funds and save some money.

I can imagine Reform articulating a version of this that would be very popular with its supporter base. That gets you to maybe 20-25% of the electorate. If the Conservatives got onboard that would double, and we can already see Kemi Badenoch steering her party in a different direction on Net Zero. Therefore it would not take much to develop a ‘common sense’ sounding attack on ESG that had strong political support.

So how to respond? Of all the tactics we are likely to hear proposed for pushing back against these attacks, trying to frame RI as largely a risk management exercise strikes me as likely the weakest. Let’s leave aside the obvious point that ‘We agree to pretend there are no political considerations in the ownership and control of companies’ is likely not the strongest position to adopt in the face of a successful counter-movement which is political to its bones.

For one, this will involve getting dragged even further into the weeds of whether or not the available evidence supports categorising Issue X as an investment risk. This type of exercise never ends.

My larger problem is that it is an approach that sees the problem as legitimacy within a narrow band of professionals. I think that risks further diminishing the constituency that might support and defend RI as a worthwhile project.

I don’t know if people advancing this type of approach have met any beneficiaries recently. My experience is that effective risk management is not top of their list of interests.1 To be honest I feel the same way. I’m going to make a shocking admission here: what drew me into the RI world was not my enthusiasm for effective risk management in the pursuit of financial returns. I tentatively suggest I’m not the only person working in this field who thinks this way.

If the response to political pressure is to try to shrink RI down to ‘it’s really just sensible risk management’ and a focus only on clearly and significantly financially material issues I’m not sure how many would get out of bed to ‘save’ it. Why would it inspire, or deserve, more support or loyalty than LDI or smart beta or whatever other investment product you can think of?

Much as I dislike the DOGE initiative in the US it is exposing a brutal reality about what we take for granted. What is striking is that DOGE is not (yet) hugely unpopular, even though it risks wrecking things many Americans supposedly value. The relative level of support suggests to me that a lot of ordinary Americans didn’t perceive that they had a particular interest in defending the status quo. Not even the status quo that delivers social security.

Perhaps people are not paying enough attention. I expect the current level of support will fall as the real world effects become felt by more people. But a lot of damage is being done in the meantime and may be hard to reverse.

Unfortunately, far less people pay attention to RI and it is questionable how much they would feel the impact if it disappeared. It seems likely few would feel anything significant was at risk if political opponents do come for RI. Positioning RI as more narrow risk management seems to make it more likely people won’t understand why they should be concerned about it being challenged.

An alternative, it seems to me, is to broaden the constituency that feels that they have an interest in RI. As I’ve written previously, RI as practiced puts far more emphasis on environmental issues than the public does when asked about what issues businesses should be pushed on. Bread and butter issues, like what companies pay their workers or threats to their employment, get far less attention. Sometimes it even feels antagonistic. I definitely get the sense that some in the climate-y part of the RI world see the just transition as a giant stalling tactic, for example.2

This could be flipped, with a much clearer focus on ensuring that businesses were well-run in a way that delivered good terms and conditions for employees, or entailed responsible behaviour on tax and so on. This might give more beneficiaries a sense this thing called Responsible Investment had direct relevance to them.

It would also need to be driven by asset owners primarily. This is partly due to the reluctance of asset managers to take a stand, or even be perceived as doing so, in the current environment. But more importantly asset owners (for now at least) do have that direct link to beneficiaries. Being aspirational, beneficiaries might even be involved in the development of RI policies, so that there is a real sense of ownership of the approach and activity undertaken on their behalf.

It still might not work, or even if it works to some extent it might not be enough to withstand a concerted attack. But personally I think we would all stand a much better chance having the fight on ground where we can say, for example, that opponents of RI think we taking too strong a position in favour of decent wages and employment conditions for pension beneficiaries in the UK.

Obviously I’d advocate for a more ‘worker-centred’ version of RI but if you can’t stomach that at the least think about how to root RI activity in the economic reality facing beneficiaries. (If your instinctive answer to this is ‘but climate change is the economic reality…’ I don’t think you’re trying hard enough.)

Elon Musk: the passions and the interests

I’m a big fan of Albert Hirschman’s work. I’m sure a lot of better educated people than me could pick holes in it - there aren’t any equations in there for starters - but I think he was a very talented writer who got interesting economic ideas across clearly.

The Passions and The Interests is one of his more interesting books, and focuses on the way that the argument was made in favour of capitalism before it became the dominant economic model. A significant part of the book looks at historic attempts to argue that giving the powerful in society an economic stake, an interest, would make them less likely to indulge their passions by invading neighbours.

This is basically the ‘doux commerce’ argument that international trade should make war less likely. The idea is often associated with Montesquieu, but Hirschman showed that it was a relatively widespread argument in the seventeenth and eighteenth centuries. For example, he quotes the Scottish historian William Robertson writing in 1769 as follows:

“Commerce tends to wear off those prejudice which maintain distinction and animosity between nations. It softens and polishes the manners of men.”

While this might seem little more than an interesting bit of the history of economic thought, this idea did resurface when Russia invaded Ukraine. Danny Finkelstein wrote a bit in The Times that included arguments that I think would have looked very familiar to Hirschman:

“The openness of London isn’t Putin’s biggest strength, it is his biggest potential weakness. Because we have allowed many rich and powerful people to make a home here, we are able to insist they choose. Do they wish to be part of Putin’s closed Russia or of the open trading world? And the price of being part of that is to condemn Putin’s actions.”

“This is not, of course, just an argument about Russia. It’s an argument about all sorts of foreign investors and political figures. There is always a balance to be struck and an argument to be had about individuals and states. We are having one now about Saudis and football. But I think our bias should be towards openness, towards the belief that by trading here and buying here, we will rub off on other less open countries more than they rub off on us.”

Unfortunately the proposition seems, well, false. Russian oligarchs seem to have concluded that keeping quiet about Putin was somewhat preferable to falling out of a window. And the broader idea that providing the opportunity for the powerful to have significant financial interests would dissuade them from aggressive empire building looks wrong too.

Arguably Elon Musk is provides the best falsification of it. Having amassed enormous wealth he is now using this to exercise political power, including interfering in the politics of other countries, amplifying the Far Right, seeking to shape the media landscape and so on. Contrary to the original claim, his interests have enabled him to indulge his passions.

Perhaps we need to make an an exception because Musk is so rich. Perhaps there are only a handful of people who can act in this way. But the argument, crudely put, that letting people make a lot of money will distract them from things that are more damaging to society looks pretty dead.

Relatedly, I wish I could find the video I half-watched a few months back (before DOGE and all the rest of it) where a finance academic sought to defend how much Elon Musk’s incentive scheme at Tesla could pay out. If I remember it correctly, part of the argument was that if Tesla shareholders had voted in favour they must have considered it reasonable and they would have the incentive to challenge it if not. Doesn’t feel like quite the slam dunk today does it?

Of course, one could still make that argument, but presumably those doing so would accept that even in the field of executive remuneration what might be considered reasonable by shareholders could be hugely damaging to society. We might call it ‘poisoning the pie’ rather than growing it.

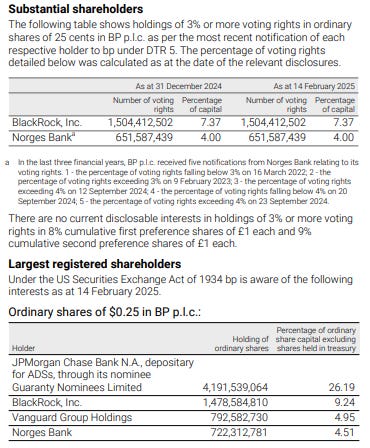

BP / Elliott, again

Did I mention that I didn’t think Elliott was a major BP shareholder? Might have.

The initial wave of stories with the suggestion that it might have up to a 5% ‘stake’ appeared on 13th February. Here’s what the FT piece from that day says:

Activist Elliott Management has become BP's third-largest shareholder after building a near-5 per cent stake worth almost £3.8bn, as it seeks to force the troubled UK oil major to cut spending on renewable energy and make big divestments, according to two people close to the situation.

Companies disclose their largest shareholders in the annual report, if they cross the regulatory threshold requiring disclosure. BP’s annual report discloses the position as at 14th February.

Well isn’t that surprising…

Who needs the beneficiaries though, right? They can’t be expected to grasp the complex issues that RI professionals grapple with. Thankfully, across the globe direct beneficiary representation in the governance of pension funds has been weakened, leaving it to the professionals to handle these issues with a technocratic mindset. We’ll have no politics here!

I spotted this recently. Obviously investors have no vested interests… but that aside, seeking to position investor engagement in policy as a “counterbalance” to “labour interests” is quite revealing.