Actually Existing Passive Management

Look at the size of it!

At the start of this year I was really pleased to be invited to speak at Warwick University on the subject of passive management. So I thought I’d turn the notes I used for that talk into a longer post.

Usual caveats apply - I’ve worked with numerous investors over the past 25 years, and spent a lot of time looking at how investors behave, but my background is in stewardship, I’m not someone who makes or has made investment decisions on behalf of others. My interest has been focused on the relationship between companies, investors and others, the distribution of rights and how they are used. With that out of the way…

Active vs passive

To start, I think an obvious but critical point to always have in mind when thinking about passive investment is that it is a fundamentally different beast to active management. Therefore we should have different expectations from the outset.

At its most basic level, active managers research and select individual stocks, with the intent to outperform a given benchmark. In practice they might hold a subset of an index like FTSE100 or S&P500, or underweight stocks in those indexes relative to the index. But active choices are made.

In contrast, passive managers hold a predetermined set of stocks, typically comprising an index, in order to achieve a market return - they simply pass on what the chosen universe returns net of (low) fees. The vanilla version is exposure to a full index weighted by market cap, but there are lots of variations.

The passive manager’s client is not expecting the manager to understand individual companies. It is expecting to achieve a market-wide return. Therefore, in turn, the manager is not going to be judged on poor portfolio selection either on performance grounds or in relation to controversies (I mean here the existence of controversies rather than the manager’s response to them). This is obviously because the manager isn’t selecting individual stocks.

The manager doesn’t have a pressing interest in the *out* performance of particular stocks because the client is not expecting the manager to identify such opportunities, and the manager doesn’t get rewarded on the basis of performance. Similarly there is no requirement to build valuation model or investment case. Therefore, there is potentially no need to utilise company reporting for the purpose of making *investment* decisions1 - stewardship decisions can be a different matter.

The case for passive management is significantly bolstered by - but not dependent on - the efficient markets hypothesis. The EMH suggests that if markets very quickly price in relevant information it will be very hard for active managers to outperform, especially net of their higher fees.2 (NB. I’m just restating EMH postulates here, these aren’t necessarily my own views.) And, because passive management is very cheap in comparison, cost has become an important consideration.

Relatedly, the EMH is based on the expectation that the reason that stocks quickly price in relevant information is because some investors are doing the hard work of assessing how developments relating to particular stocks or sectors affect future prospects and making investment decisions based on this. This should mean market prices are broadly sensible. Passive management in theory free-rides on these efforts, and accepts the prices determined by others.

When I first got interested in passive management back in the late 1990s - yes I am that old - I remember talking to an actuary at Aon called Donald Duval who pointed out that if passive management grew too large that second elements of the EMH might be compromised. There might not be enough people actively determining prices by assessing information relevant to the stocks. But at the time that seemed like an interesting theoretical point that might matter a long way in the future.

Scale

Of course, now the picture is more complicated, as passive management has grown enormously in developed markets. I’m not sure if people still use the term ‘core-satellite’ but the basic model it describes - a large chunk of passively managed equities (or fixed income I guess) run by an index manager, with smaller actively managed slices alongside - seems to have been adopted by many asset owners. This was a move away from the old ‘balanced’ (multi-asset) mandates where a pension fund might appoint one or two asset managers to do everything.

This change has shifted the balance of power in the asset management industry. Figures from the UK’s Investment Association on the proportion of passive management show it rose as a percentage of UK-managed assets from 23% to 33% in 10 years to 2023.

The growth of passive management also has a significant on companies. Most people will be familiar with the discussion of the Big Three (BlackRock, Vanguard and State Street) in the US. To just pick one stat at random As of the end of 2021, the Big Three collectively held a median stake of 21.9% in S&P 500 companies

Looking at the same issue in the UK, State Street is not such a big deal, but BlackRock and Vanguard regularly appear as major shareholders in many PLCs. Sometimes as the 1st and 2nd largest shareholders. In a recent post I showed what the picture currently looks like in a bunch of UK retailers.

Governance issues

This in turn has numerous implications for corporate governance. When I first started working in this field the investor conception of things was built upon the Bearle and Means view of the separation of ownership and control (leaving aside the inaccuracy of ‘ownership’ as a term). However, the growth of passive management means that, for many companies, ownership of their shares is being re-concentrated.

This comes after a period when public policy in many markets has sought to grant increasing rights to shareholders, such as the ability regularly elect directors, approve executive remuneration (or not) and so on.

It’s also worth noting that there are certain rights that only larger investors can exercise. You need 5% of the issued shares to call an EGM or file a resolution on your own, for example. In recent history that might mean that only an investor that had built a large position in a target company was likely to do so. But the big passive managers might have a lot more opportunities to do. BlackRock would meet the threshold in most of the retailers I looked at and Vanguard would in a few.

And it’s not just been about rights. There has been significant focus on ‘stewardship’ as a responsibility of shareholders since the financial crisis. In combination, the expectation is that large shareholders should be actively involved in the companies whose shares they hold.

In practice, the scale of their collective influence doesn’t seem to change their conception of voting and engagement, but should it?

Executive pay

Executive pay is an example where there might be a reason for passive managers to approach the topic in a fundamentally different way (this following section is largely based on something I wrote previously, full version here).

The position of an active manager is reasonably straightforward. The relative and absolute performance of their portfolio companies is what they live and die by. If there are, say, half a dozen companies in a particular sector and they have a position in only one or two of them then decisions about executive pay flow from this. Evidently they want the companies they hold to flourish rather than those that they don’t.

Therefore if they believe it is necessary to pay highly to recruit and retain the best talent they will be inclined to do so. They may consider that there are only a handful of people qualified and skilled enough to be suitable CEOs, for example. Therefore they will want those people working at the companies in which they have a position, rather than those to which they do not have exposure.

Passive managers are not in the same position. In the most simple version of the product they are primarily judged by their ability to deliver a market return at low-cost. If any individual stock or sector underperforms the manager will not be judged negatively for having chosen to hold it, they are holding it because the client asked them to by seeking exposure to a particular index.

Now presumably passive managers also believe they should act in their clients’ best interests by not supporting any value destructive behaviour by investee companies (although their ability to effectively monitor for this is obviously challenged by the sheer number of companies held).

So how should this inform their orientation be towards executive pay? Why should they support paying more to secure executives at companies 1 and 2 but not 3, 4, 5 and 6? They could support paying more for executive talent at all companies. This would impose a portfolio-wide cost increase and would essentially be a bet on the idea that this would result in a market-wide improvement in performance.

This has been recognised by managers themselves. Way back in 2010 the then Conservative-Liberal Democrat coalition government undertook a consultation on short-termism titled A Long Term Focus for Corporate Britain which included some questions about executive pay. Blackrock’s submission included the following:

One of the difficulties we face as investors is that we (rightly) assess a company’s arguments for pay changes or increases in light of that company’s circumstances. Generally, companies do present strong arguments for the changes they wish to make. But our assessment tends not to take into account the impact it will have on the trend overall.

I think this works better as a justification for an active manager - we only hold a subset of the market, so we don’t really look at the impact market-wide. But if you are large passive manager you hold the market. It feels a bit odd if you don’t look at the overall impact. Shouldn’t a manager that holds the market think from that level down, not from the portfolio company up? If your mandate is deliver a market return then if there is a tension between what would be be beneficial to an individual company and what would be beneficial to the market as a whole, should you favour the latter? Perhaps paying more at companies 1 and 2 improves their performance relative to 3, 4, 5 and 6. But if restraining pay across the sector achieves a greater combined return across all six should the manager choose the latter?

Perhaps a passive manager’s view should be:

we (rightly) assess a company’s arguments for pay changes or increases in light of the impact it will have on the market overall rather than that company’s particular circumstance

It is obvious that passive managers do not currently approach the executive pay topic like this. But it’s not immediately obvious to me why they shouldn’t or, less ambitiously, why they should not at least consider the aggregate impact of individual company decisions.

On both sides of M&A

If executive pay is problematic, other issues aren’t any easier. Another topic that has interested me for a while is how passive managers think about M&A.

Because of market-wide exposure, passive mangers may hold both target and acquirer in certain takeovers, and they do so only because of the mandate from clients to gave exposure to the given market/index. Because they did not make a decision to hold the target or the acquirer, and are not paid on the basis of the performance of individual stocks, the price offered is not as critical as for an active manager holding the target.

But given that the passive manager is a shareholder - often one of the biggest shareholders - they have to make a decision, so how do they do it?

This is from the latest iteration of BlackRock’s global investment stewardship principles:

In assessing mergers, asset sales, or other special transactions, BlackRock’s primary consideration is the long-term economic interests of our clients as shareholders. Boards proposing a transaction should clearly explain the economic and strategic rationale behind it. We will review a proposed transaction to determine the degree to which it can enhance long-term shareholder value. We find long-term investors like our clients typically benefit when proposed transactions have the unanimous support of the board and have been negotiated at arm’s length. We may seek reassurance from the board that the financial interests of executives and/or board members in a given transaction have not adversely affected their ability to place shareholders’ interests before their own. Where the transaction involves related parties, the recommendation to support should come from the independent directors, a best practice in most markets, and ideally, the terms should have been assessed through an independent appraisal process. In addition, it is good practice that it be approved by a separate vote of the non-conflicted parties.

So decisions will be with an eye to the long-term economic interests of clients, which I think we can assume that for practical purposes this once again means ‘price’. It is not clear how the manager arrives at a figure if at least some clients are on both sides of the deal. In reality a manager like BlackRock will have thousands of clients spread across hundreds of funds so this must be a common occurrence.

To put this in perspective it’s well known that a common merger arbitrage strategy is long the target/short the acquirer because of the expected impact on the valuations of both. Admittedly this is a relatively short-term strategy - the duration of the bid and its completion - but it does demonstrate that an investor holding everything must find it hard to make the decision on behalf of clients on the basis that the price being offered for the target is a good one.

In addition, the stated policy makes it sound like the manager plays a passive role in any takeovers. The offer comes in and the manager considers it in light of client interests and with some consideration of governance issues relating to the bid.

But reality seems to be somewhat different. When Anglo American was the subject of a bid from BHP there was a piece in the FT claiming that BlackRock had been encouraging the Anglo American board - which has rejected BHP’s various offers to date - to hold “meaningful negotiations” with BHP. That does not look like an investor playing a passive role during a takeover.

These are not easy issues. On the one hand, it does feel somewhat incongruous for passive managers to be playing an active role in takeovers given that their positions in companies derive from client decisions that I do not think mandate this. On the other, if these managers are the largest shareholders in many companies that are or could be subject to bids it would also feel odd if they made black box decisions. The whole area really deserves further scrutiny given what is at stake.

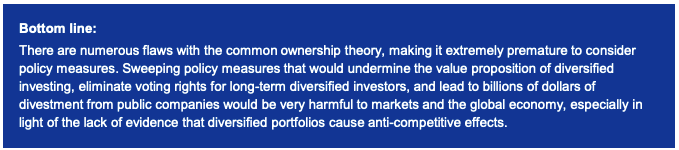

Competition and common ownership

A third area worth considering in relation to ownership issues relates to passive managers having become large shareholders in companies across an industry. The impact this could have on competition - where an investor or group of investors hold all the players in a sector - is the focus of the ‘common ownership’ theory. The short version of this idea is that because all the firms share common ‘owners’ there is reduced incentive for them to compete against each other rather than finding other ways of delivering value to the investor(s).

I can’t remember who said it, but the ‘common ownership’ theory has been described as the ‘evil twin’ of ‘universal ownership’, which I think makes a lot of sense. In a sense, my argument that in theory passive managers ought to think about executive pay at portfolio rather than stock level is a version of this.

It’s a slightly odd theory, but it has worried the big US passive managers to the extent that it now shows up as a risk disclosure in BlackRock’s annual report (this section also addresses the obviously linked issue of the scale of indexing).3 Because I’m a nerd, I’ve been tracking the word length of this disclosure and it steadily rose since first appearing in the 2017 annual report… until 2024.

It’s always worth a read as there is usually a useful nugget or two about regulatory developments. For example this is from the most recent annual report:

[I]n 2024, the FTC and DOJ submitted a joint comment letter to the Federal Energy Regulatory Commission (“FERC”) encouraging FERC to consider common ownership as a relevant factor in updating regulatory relief available to asset managers.

I had missed this, but I tracked down the relevant letter which dates from April 2024. The interesting thing about this as it shows significant regulatory interest in the topic under the Biden administration. The FTC and DOJ under Trump has just sought to intervene using the common ownership argument in relation to the passive managers influence over coal companies.

It’s not surprising also that concern about common ownership has appeared in regulatory guidance on mergers and acquisitions.

The overriding point here is that competition-related concerns resulting from indexing may only be starting to find practical application in policy. The fact that the scale of influence of passive managers in relation to competition issues has raised very different concerns from both the Left and the Right ought to tell us something. The core critique is the same.

Are some passive managers even holding the stock?

A further element of the passive management business to think about is the extent of stock-lending. Index managers - and their clients - can make solid income from stock-lending. In some ETFs the management fee has been zero when set off against lending income. It’s decent business for the manager to be in - using the client’s money to buy stock that you then lend to a third-party for income - but since the client gets the lion’s share of the income derived no-one is complaining.

Stock-lending is a market in its own right, and that throws up some incentives that may make governance types a bit queasy. The more restrictions you put on your stock - like the ability to recall in order to vote vote, or standards for collateral - the less likely you are to be tapped up first by the party arranging the loan. So loaning for long periods – term trades - is more valuable. In practice stock can end up on loan for prolonged periods, during which time the collateral the lender holds might be quite different to what they have lent, as I’ve shown previously with ETFs. Similarly, since it’s about supply and demand, the lender will be able to ask for more to lend out in demand stocks – for example where a lot of investors want to short the issuer.

The thing that has interested me is whether stock-lending should alter stewardship activity. If you are a 10% shareholder but loan out 5% should the issuer treat you as a 5% holder? I think the answer is probably yes, but in practice I’m pretty certain most investor relations people would not want to risk it.

How are the big managers responding?

In conclusion, there’s a lot there, and an obvious question is the one above. I think this initial response from the biggest passive managers has been to make themselves look as unthreatening and inert as possible. Personally, I’m not sure this is going to be successful over the medium term but it seems to be where we are.4

It’s a commonly held view that, because of the political pressure being exerted on them, the commercial incentives for US passive managers have changed and this has led to shifts in behaviour. At a trivial level, as is well known, ESG material and language has been removed from websites, presentations and so on.

More significant are shifts in policy and in practice. Until around 2021 there was an upwards trend in voting on ESG proposals but this has clearly reversed, with the Big Three all cutting back votes in favour in the last few years. Vanguard is clearly the least supportive, followed by BlackRock with SSGA slightly better.

I find this fascinating, given that many commentators (rightly in my view) draw a line straight to the influence of Republican-controlled funds. When I first got interested in this field the idea that corporate clients might quietly threaten asset managers with loss of business to dissuade them from voting against was sometimes raised. But I very rarely heard examples of it and in any case at that point we were in period when shareholder engagement was starting to seriously take off.

What we have seen in the last few years is this client power being explicitly and publicly used to shift asset managers, successfully. Whilst in the last few years this has been undertaken by opponents of ESG, it is also exactly what pension funds have been encouraged to do for years in order to make asset managers more supportive of social and environmental issues.

We can also see the willingness to limit involvement in the business of investee companies in the passivity agreements that have been put in place between some managers and regulators. The Trump administration does not appear to be shy about pressurising the private sector to support its objectives. I do wonder if they might look at expanding the scope of agreements like this.

Finally, another way that asset managers have tried to ride two horses is by trying to give power away by allowing individual clients to direct voting themselves - pass-through voting. Again I’ve written about this before and won’t rehash the pros and cons. But it should be noted that BlackRock was developing this functionality before the anti-ESG wave hit. So perhaps this was driven more by a desire to address concerns about common ownership and the scale of indexing, which had emerged earlier. All the Big Three offer versions of this now.

Looking from the outside, the over-riding message that the biggest index managers seem to be conveying is that they don’t really want the power they have and will cede it to clients or simply not exert it if that helps avoid controversy.

As I said, I’m not convinced this will work, since the practical outcome would seem to be the creation of a huge inert bloc of share ownership. That would surely invite questions about shareholder primacy.5

The bigger point is, well, bigness. Mega managers trying to play dead does not remove the fact that they are huge. The question that remains is whether that scale is a problem in itself or not.

In my corner of the world I still don’t see much discussion of this, even as it is starting to bite as a regulatory risk factor. I think this is partly because we are still grappling with the implications of reversals in asset manager commitments and activity in relation to ESG topics. As responsible investment grew, it made sense to try and influence/move the largest blocs of capital because that would in turn influence investee companies. Now that we have rolled back down the hill somewhat does the same approach still make sense, or should we be at least as interested in breaking up concentrated power?

There is a whole subplot here, as both Barclays and Standard Chartered are trying to bump passive investors out of litigation on the basis (my huge simplification here) that they can’t have been misled by information that they didn’t use to inform their acquisition of a shareholding (known as ‘reliance’). The judgments in these cases point in different directions currently.

Another view might simply be that forecasting (which is what much investment decision-making really is IMHO) is really hard given we are dealing with an unknowable future. Another book that had a big influence me is Expert Political Judgement by Philip Tetlock as it shows how poor we are at guessing the future (some of us are worse than others). Coincidentally, on the penultimate page of the main text in my copy he compares resistance to trying to assess political forecasting (which would demonstrate how poor it is and who is better/worse at it) to resistant to index funds!

BlackRock also used to have a section on its website where it posted research dedicated to challenging the common ownership theory. Here’s a good example from 2019, BlackRock’s conclusion was pretty clearly aimed at discouraging policy interventions.

There’s a nice video here tackling the (in my opinion wrong-headed) question of whether ESG is being politicised which grapples with the choices faced by asset managers. A key point towards the end is that because asset managers have power whatever they do is political. To embrace RI/ESG is political, but to retreat from it is also political. There is no escaping this because….

Whilst challenges to shareholder primacy have normally come from the Left, in the current environment of increasingly powerful illiberal movements of the Right one could envisage something similar coming from there. Whilst the former will be concerned about the lack of accountability arising from large investors not using their rights as a countervailing power, some from the illiberal side of politics might question what these rights are for anyway.

Thinking practically, could we head towards a corporate governance version of the ‘consumer welfare’ orientation of competition policy? If boards are already delivering in the interests of shareholders should they face any restrictions, and do those shareholders really need tools to achieve that outcome? Shareholder interests could still have primacy even if shareholders played no role in creating that outcome. So a ‘shareholder welfare standard’ if you like.

Incidentally I think this is not miles away from a view of the world Alan Greenspan was endorsing years ago here: “[I]f the owners are no longer the managers, CEO control and the authoritarianism it breeds are probably the only way to run an enterprise successfully. There do not appear to credible alternatives to placing the power of governance in the hands of the CEO...”