Pass-Through Voting

Pass-Through Voting (PTV) has become a regularly discussed topic in the governance and stewardship world. I’ve always personally been favourable to the idea for some quite specific reasons.

Years back, I was a trustee of a pension fund where the beneficiaries had a very clear set of of views that the fund wanted to give expression to but that no asset manager was ever likely to align with. So there was no question of picking a better manager (regardless of how important voting would be in a manager selection process in any case). I know a number of funds were in the same boat and were also investing via pooled funds1, so we were all simply stuck with votes being exercised in a way we didn’t agree. That really informed my view going forward.

Later I worked with a shareholder advisory firm, so PTV obviously held commercial interest. But these days I don’t have a direct personal or commercial interest and my views haven’t really changed. That said, I recognise there are a number of good faith criticisms of PTV that aren’t easy to dismiss.

The Investor and Issuer Forum has just published a really nice research report on PTV which you can access here. I think it’s a really even-handed report on some of the drivers of PTV, and the variety of views in the market.

It’s interesting to note that there isn’t one view that comes from either asset owners or asset managers. There are pension funds that want to direct their own voting because they have a well-established stewardship approach that they want to apply consistently. Others consider that the most effective stewardship is achieved by appointing managers with aligned views. Similarly, it’s clear many active managers are instinctively resistant to PTV because they consider stewardship is part of their overall investment approach. Conversely, some of the US managers seem to want to get their clients voting and see PTV as an important part of client servicing.

Issuers appear to predominantly have concerns about PTV rather than see benefits. Concerns cited include the increased difficulty in engaging investors and that PTV might increase the influence of proxy advisers.

As an aside one pro-PTV argument I would add (and that is one of the reasons I am supportive) is that it would help tackle the (unintended) concentration of power in the hands of the big index managers. I think this is is preferable to other proposed solutions to this like a cap on the amount of shares that a manager should be allowed to vote.

This is more of a political economy take on the issue, which is why it doesn’t tend to appear when the discussion is only between investors, companies and those that advise either. So it is worth remembering that others have a legitimate interest. Especially given that the policy world’s interest in scale, and common ownership, has clearly influenced some of the things coming out of the US.

The report concludes with a number of proposed principles for PTV. As I say, it’s a really balanced and informative piece of work so definitely worth your time if you have any interest in shareholder voting.

How big is PTV?

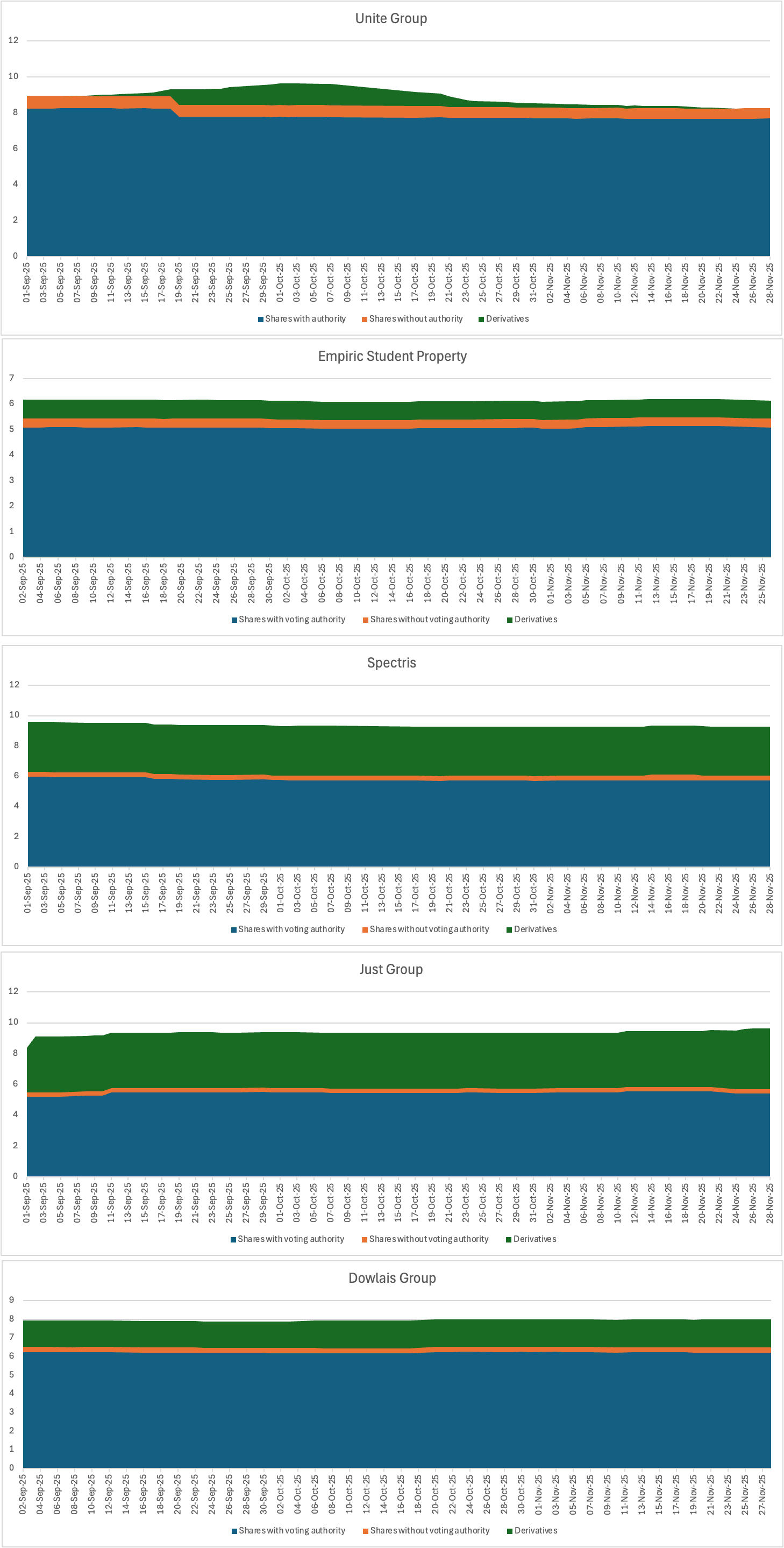

I have a bit more to add myself. The report also says that PTV hasn’t achieved significant scale as yet and therefore is unlikely to have an impact on voting outcomes except in rare cases. As covered in previous posts, I’ve been looking at regulatory filings relating to voting rights. The footnotes on certain BlackRock filings *might* provide some indication of the scale of PTV. As noted previously, these indicate the number of shares where BlackRock does not have authority to vote.

A well-deserved hat-tip to David Akinyele-Aje who has helped me scrape a load of BlackRock filings to get a better picture of this. The charts below pull info from 8.3 forms issued between September and November 2025. These are all companies involved in takeovers and the charts show BlackRock’s economic interest through shares and derivatives in each company.2 The orange segment in each chart represents the shares (as a % of the issued share capital) where BlackRock does not have voting authority.

With David’s help I’ve got hundreds of these filings covering a bigger set of companies, so these are just some examples. As you can see, the proportion of shares without voting authority is small, but it’s not nothing. Looking at all the filings (relating to about 30 companies) over the three months the average % of the ISC where BlackRock did not have voting authority was about 0.3%. The highest was around 0.7% for a UK company. However the disclosure regime also captures some information on takeover parties that aren’t UK based. I can see a disclosure linked to a US company where the level of shares without voting authority hits 0.92%.

Remember that we know that turnout regularly drops at PLCs during takeovers meaning that those who do vote see their power increased. To take the recent example of the Wood Group, if 0.3% of the ISC was voted in a meeting where the turnout was 22% this scales up to a 1.36% vote at the meeting.

To be clear: I do not know that the disclosures in the BlackRock filings do reflect PTV. I observe that these disclosures only started appearing routinely a year and a bit ago and that shares held by a manager but subject to PTV could be reasonably categorised as the manager not having voting authority.

Regardless of whether it is PTV or not, it is evidence of a non-trivial slice of the ISC of companies involved in takeovers being held by BlackRock but apparently being voting elsewhere, systematically.3 I plan on doing some more analysis of this issue which I’ll write up in 2026.

My own ongoing research is not about PTV per se, but about how voting authority fragments during control events (which outsiders might consider to be a time when stewardship interest ought to peak). I think the governance and stewardship world has a bit of a blindspot here currently, lacking both a framework for understanding the mechanics (and the implications that arise from common practices) and data to establish what actually happens during the process.

If you’re working through similar issues around voting authority, stewardship during takeovers, or PTV in practice, I’m always interested in comparing notes.

The funds weren’t big enough to try and negotiate the type of ‘carve out’ that some have managed to put in place.

The use of derivatives is something else I want to dig deeper into.

Obviously BlackRock is not the only manager offering PTV, and I’ve also identified other managers making similar ad hoc disclosures about lack of voting authority for part of their shareholding. It’s another angle I need to explore.