Materiality, conflicts and scale

A couple of post-CII reflections

I was very pleased to be at the Council of Institutional Investors spring conference this week, moderating the Railpen and Predistribution Initiative meeting on workforce directors. It was a great meeting, and we had lots of discussion with people throughout the conference about the idea of broadening participation in corporate governance.

One of my questions to the panel was whether opponents of workforce directors believe that it wouldn’t change much, or if their concern is that it would change too much. Caroline Escott at Railpen was, I think, dead right in her response that actually most people haven’t even thought that much about it. Rather there is a bit of a kneejerk reaction against the idea.

I think underlying some opposition is the idea that workforce directors might try to shift decision making in an inappropriate direction. This is implicitly a recognition that there are competing interests within the firm, and that opens up a rather important question that is also sitting under discussions about financial materiality and shareholder engagement.

By way of context, the over-selling of ‘win-wins’ within RI is clearly over. Indeed increasingly investors are urged to be very clear on what issues they can’t take a position on (unless mandated by a client).

If shareholders can only legitimately engage on issues where there is a clearly financially material case this has a couple of knock-on effects, one that is discussed in the stewardship world, the other we largely keep quiet about.

Firstly, it means that some issues that are very material for stakeholders, but do not offer positives for investors, must drop off the stewardship agenda. Secondly, however, those issues don’t disappear. The advancement of topics that would benefit stakeholder groups but are not positive (or are even negative) for shareholders no longer features within stewardship activity. But it does not follow that those topics should not feature within decision-making within the firm.

The question will inevitably arise “why should shareholder interests predominate?” (btw If you’re tempted to respond “because shareholders own the company” I’m happy to share details of my career-long turn away from this beguiling but fundamentally false claim, with a slide deck if need be! )

The more that stewardship paints itself into a corner on financial materiality and ‘this is just about risk management’ the more likely it is that shareholder primacy comes back into focus as a contestable idea. Rather than becoming a channel for change, the role of investors may become regarded as irrelevant, or even as a blockage. The alliances that formed between civil society and investors over the past couple of decades or so may turn out to have been historically contingent.

I suspect that many people on the investor side of the equation may not be concerned about this currently. Less nagging emails and calls from NGOs, right? OK, but in a moment when shareholder rights are being curtailed it should not be surprising if there is a lack of allies when trying to reassert them.

Whenever you speak to ‘ordinary’ beneficiaries it is a useful reminder that no-one is born believing in shareholder primacy and all it entails. It has to taught/learned. Most people do not instinctively feel that action on social and environmental issues must be underpinned by the existence of demonstrable financial returns to investors. This has always been the fundamental tension lying underneath governance and stewardship. It may yet return to the surface.

Pass Through Voting - tackling the elephants in the room

I also heard various people at CII talking about Pass Through Voting (PTV), something which has shifted from an interesting idea to a functioning product with growing take up in just a few years. In common with opposition to workforce directors, there continues to be some instinctive hostility. Though in the case of PTV practice is now bypassing theoretical objections.

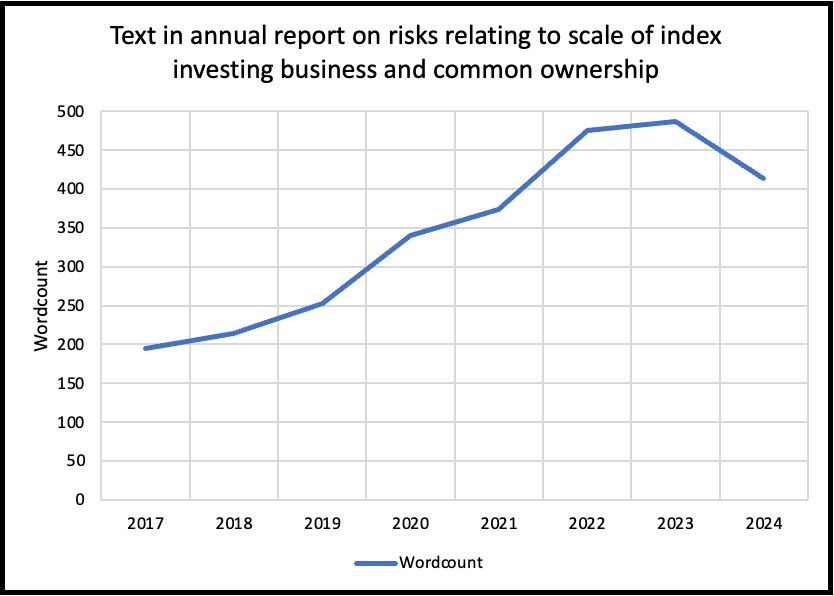

One thing that always jars with me is when I read/listen to something about the case for and against PTV that does not address the issue of market concentration. BlackRock was developing Voting Choice before the anti-ESG wave kicked in. I believe this is because it was intended in no small part as a response to concerns about concentration of voting power. BlackRock started disclosing concerns around the scale of indexing and the related issue of common ownership as a risk factor in its annual report in 2017. Since then its disclosure on this question has grown and has included references to relevant regulatory interventions.

I think there is generally silence in the governance/stewardship world on the scale question for a number of reasons. First, to borrow Caroline’s insight, I think maybe people just haven’t really thought about it a lot (perhaps because there is no incentive to). Second, relatedly, this corner of the world does tend to like doing what it has always done. Client alignment and mandate design are the kinds of things people already know how to do. Tackling market concentration, not so much. Third, at a theoretical level, I think there is some attraction to the idea of investors having big positions in companies to bring about change (though this model never envisaged the same handful of investors having large stakes in all companies).

I’ve written recently about democratisation. Unfortunately, I think opposition to PTV can inadvertently end up on the wrong side of this. There has been a tendency to think that the big prize is to move the largest managers to adopt better positions and/or engage more forcefully. For some, this was all well and good when the biggest managers seemed to be moving to more ‘progressive’ positions. Only when the wind changed and those managers started walking back did it become apparent why that might be a problem.

Personally I am not at all in favour of governance and stewardship model that involves moving concentrated blocs of voting power. To state my own position clearly: even if BlackRock and Vanguard achieved the impossible of being perfectly aligned with their clients, and even if they adopted a set of policy positions I agree with, I would still think them controlling 15% of numerous major UK PLCs would be a problem.

Clearly this is a widely shared view. Bernie Sanders and Vivek Ramaswamy don’t agree on much, but they both see a problem in concentrated voting power in public companies. There are a lot of people who look at this issue from the outside and perceive a problem. Yet it receives little discussion within the governance and stewardship world even when the topic is dispersing voting concentration! That just does not seem serious.