A Living Wage - the Next best thing?

A quick flick through Next PLC's annual reports

AGM season in the UK this year is going to include a focus on the need for the real Living Wage in the retail sector. Co-ordinated by Share Action, investors have filed resolutions at Next, Marks & Spencer and JD Sport. Next will be first to the vote - its AGM on Thursday 15th May.

The request to the company in the resolution is as follows:

To provide investors with the information needed to assess the Company’s approach to human capital management, shareholders request that the Board and management oversee the preparation of a report outlining:

1. The Company’s approach to setting base pay for hourly paid direct employees and which committee of the Board has oversight of this;

2. Number of direct employees whose base pay is below the real Living Wage, broken down by contract type (permanent or fixed-term) and working hours (full-time, part-time or non-guaranteed hours employees);

3. Hourly paid direct employee turnover rates, broken down by base pay and working hours (full-time, part-time or non-guaranteed hours);

4. The Company’s approach to setting base pay for regular, on-site, third-party contracted staff and which committee of the Board has oversight of this;

5. Number of regular, on-site, third-party contracted staff whose base pay is below the real Living Wage; and

6. Cost/benefit analysis of implementing the real Living Wage as a minimum rate of pay for direct employees and regular, on-site, third-party contracted staff.

So in this post I’m going to look at the context in which the vote will take place, drawing on Next’s own annual reports. All the information relating to Next used in this post is from its own reporting.

Next reporting

At a general level, the company’s reporting is quite stripped back. It generally eschews a more ‘narrative’ approach and is surprisingly light on imagery, given the market it is in.

Next does not provide information in the current annual report on relationships with trade unions. In previous reporting it has referred to recognising USDAW in respect of some warehouse and distribution staff. But there is no information on to what extent collective bargaining currently determines pay within the company, if it does so at all.

Next also does not disclose any specifically workforce-related principal risks in the latest annual report. It does refer to labour disputes in Bangladesh, but that is under the broader ‘Key suppliers and supply chain management’ risk. As a comparison, many companies identify recruitment and retention of staff, or some variation on this, as a principal risk.

Turnover

This last point is relevant to considering how to vote. While the resolution is primarily focused on pay, and specifically the Living Wage, it also seeks disclosure of turnover data. It is clear that Next captures and monitors this type of information. On page 112 on the latest annual report it refers to “Monitoring absenteeism and employee turnover”. On page 130 the remuneration committee report states:

“Along with the employee forum feedback, earlier this year the Committee reviewed and discussed a range of ‘dashboard’ information on important employee matters such as pay and reward, bonuses, benefits, diversity, equality of pay, internal promotions, culture and behaviours (including data on staff turnover by business division, absences, redundancies, disciplinaries and grievances), and learning and development.”

However, in the annual report the company does not currently provide any of the turnover data that it captures. Although it is not mandatory to report such information, a significant number of FTSE350 companies do so voluntarily.

Notably the ISSB project on human capital management reporting found this to be an area where investors want more information:

several specific data points emerged as consensus priorities for investors, including information about worker turnover, and the structure and composition of the entity’s workforce and its supply chain;

Pay dispersion

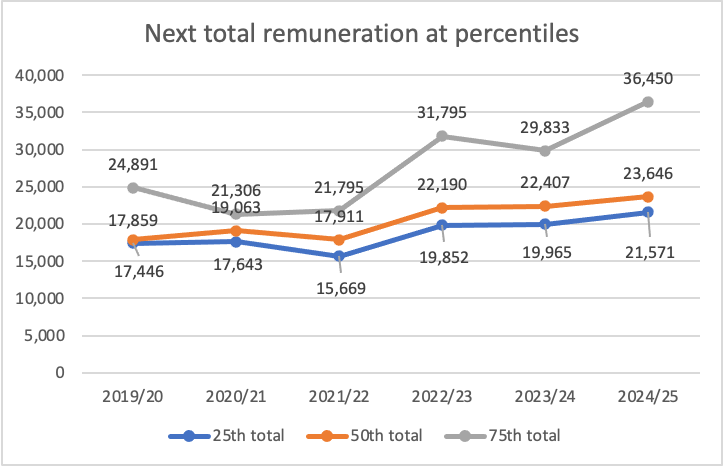

Now let’s look specifically at pay. Under the pay ratio reporting requirements, Next has to report salaries and total remuneration at the 25th, 50th and 75th percentiles. I personally find this more interesting than the ratio itself, and these figures are particularly informative when considering the resolution.

Next uses ‘Option B’ to calculate these numbers, described as follows.

We have used option B in the legislation to calculate the full-time equivalent remuneration for the 25th, 50th and 75th UK employees, leveraging the analysis completed as part of our most recent UK gender pay gap reporting as at 5 April 2024. As we have a very significant employee base, NEXT has chosen to calculate its Chief Executive pay ratio using this data as it was felt to be the simplest and most robust way to identify representative employees in the organisation at lower quartile, median and upper quartile.

The employees at the median, 25th and 75th percentile were identified using the 5 April 2024 gender pay gap data and were also in employment at the year end in January 2025. We have used their base contract salaries for the 2024/25 financial year, grossed up to the full-time equivalents, to which we have added actual benefits, bonuses, long term incentives and pension (if applicable). The data points are reflective of our Company structure and types of roles across the organisation and accordingly the Committee believes the median pay ratio for 2024/25 to be consistent with the pay, reward and progression policies for the Group’s UK employees taken as a whole as at the reference date. We consider that these ratios are broadly appropriate in the context of comparison with other retailers.

The base salary and total remuneration received during the financial year by the indicative employees on a full-time equivalent basis used in the above analysis are set out below. The reference date for determining the pay and benefits figures is the year end date.

The two charts below show the changes in salary and total remuneration at those percentiles from 2019/20 to 2024/25.

Next is a high street retailer so salaries and total remuneration are lower than we might see in other sectors. As a reference point, the ONS estimates that median gross annual earnings for full-time employees were £37,430 in April 2024. It appears that more than three quarters of Next employees are paid below that level.

More specific to the resolution, the real Living Wage as an annualised salary is £24,570 and the London Living Wage is £27,007.50. So, it appears that half the workforce is paid below that level. Reporting by Next as requested by the resolution would be able to confirm this.

At a more general level, over the period, reward for a worker higher up the income scale, at the 75th percentile, looks to have risen more quickly than for those in the bottom quarter, and this is true for both salary and total remuneration.

Costs of key management personnel

Next’s annual report also provides information on reward for its leadership. The chart below uses data from the notes to the financial statements for costs of key management personnel – in this case the directors of Next Plc.

Again, expenditure on key management personnel appears to have risen more quickly than salary or total remuneration for the typical employee at the 25th percentile.

On the face of it, then, remuneration within Next may have become more unequal over the period, with apparently significantly greater increase in reward both in the boardroom and at the 75th percentile than at the 25th percentile.

Relative importance of spend on pay

As required by reporting regulations, Next also provides a comparison of expenditure on the workforce to distributions to shareholders via dividends and buybacks. This information for Next is summarised in the following chart.

After ceasing buybacks during the Covid-19 pandemic, in common with many companies, Next has subsequently made significant distributions to shareholders via both dividends and buybacks.

Whilst this data sometimes interpreted as the relative split in rewards to employees and investors this misses an important distinction. The expenditure on the workforce is necessary in order for the business to function and achieve its objectives. After this, if the company is profitable, it can make distributions. This is why shareholders are considered to be residual claimants. The reverse is not true – distributions to shareholders are not necessary in order for the business to achieve operational objectives.

The overall picture at Next is of a company which is performing well and therefore able to make regular and significant distributions to its shareholders.

Use of third parties to determine reward

Finally, it is worth considering one of the company’s arguments against the resolution. In its opposition statement, Next makes the following claim:

“Accreditation would transfer responsibility for annual pay adjustments to an external third party — the Living Wage Foundation. This would limit our ability to adjust pay based on Company performance, specific circumstances, and the needs of our colleagues and investors.”

Here are a few points to consider in return. First, the resolution does not actually ask Next to seek accreditation, but rather to enhance reporting on pay practices and turnover, in addition to cost-benefit analysis of implementing the real Living wage. So, whatever the merits of this argument, it does not directly address a request made in the resolution.

Second, Next is already required to adhere to the national minimum wage, which is also largely determined by an external third party – the Low Pay Commission. Essentially adopting the Living Wage raises the floor, above which employers still have the flexibility to negotiate specific pay rates.

Thirdly, Next's annual report shows that it already pays external third parties to advise it on reward practices. The company’s remuneration report states:

The Committee engaged FIT Remuneration Consultants LLP and FIT Remuneration Implementation LLP (together FIT) to provide independent external advice, including updates on legislative requirements, best practices, and other matters of a technical nature and related to share plans… Deloitte LLP provided independent verification services of total shareholder returns for NEXT and the comparator group of companies under the LTIP. Deloitte provides other consultancy services to the Group on an ad hoc basis. FIT and Deloitte were appointed by the Committee based on their expertise in the relevant areas of interest. During the year FIT was paid circa £32k and Deloitte was paid circa £6k for the services described above, charged at their standard hourly rates.

Generally, remuneration committees utilise such consultants to provide information on the reward necessary to attract, retain and motivate senior leadership. The Living Wage Foundation provides information on the minimum reward necessary for employees to enjoy a decent standard of living. Although these are different objectives, it’s not obvious to me that there’s a significant point of principle at stake here in deferring to the expertise of third parties.

Overall, it’s not a given that Next’s current pay structure is the only one that would enable it to operate successfully, reward the workforce fairly and make sizeable distributions to shareholders. In recent years its approach – whether deliberately or not – appears to have increased pay dispersion, with reward increasing more slowly lower down the income scale.

Perhaps this approach leads to more turnover lower down the wage scale. Perhaps increased reward at lower levels would have seen the company be equally operationally successful, and in a way that would have enabled more of Next’s workforce to fully enjoy the fruits of that success. The annual report does not provide enough information to enable investors to determine if that is the case.

Therefore, disclosure of the information sought by the resolution would be very valuable.